Ops leaders struggle to assess customer demand related risks in real time. This increases revenue risk. This is a bigger issue amid rising uncertainties like tariffs and inflation (circa 2025). Learn one of the many ways how Zyom helps customers such as Cambium Networks tackle Revenue risks.

Most Operations leaders can’t answer in real time, or even near real time:

Which portion of my planned customer demand is at risk this quarter?

Which orders are at risk?

“At risk” here implies a significant likelihood that customer orders would not materialize, or even if it does, cannot be shipped on time.

Changing signals make it impossible to get demand and supply plans aligned, even using well-crafted spreadsheets and sophisticated, but siloed systems — planning cycles drag, errors creep in, critical Revenue and cross-functional meetings and forums (such as Sales & Ops Planning or S&OP) result in more unanswered questions, and by the time the risks are visible, revenue is already slipping away, or worse (orders lost to competitors).

In times of “garden variety” uncertainty these questions to uncover risk are hard to answer. In an environment of high uncertainty such as now (starting circa Q4 , 2024, to late Q3, 2025 in the US), identifying demand risk has become increasingly frustrating. Largely due to tariffs and pressured trade relations which directly impacts significant trade volumes from partners across the board (larger partners such as the EU, Japan, South Korea, and relatively smaller ones like Vietnam), these risks have increasingly grown for US based product companies. And this without taking into account the slowing employment picture and persistent inflationary trends which, in many industries, is already dampening if not damaging demand.

Branded product manufacturers like Cambium Networks cut planning cycles by 60%-80% and gave key executives and operating team members direct line-of-sight into supply risk with Zyom, starting in 2017. Their SVP of Ops called it “a system that brought our vision to fruition.” Cambium continues to partner with Zyom as it navigates demand corrosive uncertainties.

If you can’t see revenue at risk until the quarter’s target is already slipping, and key operating team members are scrambling to get supply inbound, you’re too late.

Key Questions for COO and Operations team

What is one key system capability from a supply Operations standpoint that companies such as Cambium need to ensure they spot revenue risk as early as possible? How should this capability evolve?

What is one valuable decision prompt that the system can automatically provide to speed up decisions and actions from Supply Operations? This was not technically feasible prior to the advent of the newer generative AI technologies (late 2022 ChatGPT launch). i.e., traditional Machine Learning approaches till the public advent of GenAI (LLM) technologies.

To find out more, drop a comment here, or email us at: products@zyom.com

Sources & Acknowledgement: Zyom’s Cambium Networks Case Study.

John Duvenage provided key inputs to structure and composition.

Disclaimer: Generative AI was not used for composing any of the writeups on this site (including this one). GenAI was used to generate the pictures in this article and for content summarization. At this point of time, there is no plan to use GenAI to generate new content on this site. Readers will be informed in advance if this changes.

Effective inventory management is vital for companies operating across regions, especially during demand uncertainty. While healthy inventory levels provide an advantage, rising inventory levels can become a financial burden quickly. Channel inventory, in particular, can be misleading, masking underlying inefficiencies and costs. This article explores how COOs can increase a company’s focus and optimize inventory across the value network, enhancing efficiency and reducing risks that could undermine even well-run companies. UPDATE – don’t forget the Action section at the end.

In the Finance function “inventory,” as a default, is reported as a “Current Asset.” Ask those in Supply Operations. They’ll tell you that nothing could be farther from the truth. This is especially true in times when demand uncertainty[1] grows.

Managing inventory in companies that manufacture and ship products is a demanding exercise. It requires careful consideration of all the variables that impact demand and supply at various nodes of the value network (not just the supply network). Decisions have to be calibrated using data and inputs across functions – decisions, often based on approximations and imperfect information. And it must be done on an ongoing basis, otherwise important data or signals can slip through the cracks.

It becomes even more complex in cases where companies sell through channel partners (distributors, VARs[2], etc.).

Channel inventory, specifically Distributor inventory, is deceptive. Although, it is no longer on your company’s books, you are not off the hook for it either. Among many things, it depends on the skills of the channel partner in managing inventory and reordering, your contractual relationships, and other factors – such as inventory and ordering patterns across your value network.

If demand changes significantly, then orders for your products can swing up or down. Inventory sitting at your channel partners can also be returned in some cases (“stock rotation” for instance). This can lead to unforeseen reduction in your Revenue. Costs will also increase as you restock your channels with newer products and take receipt of older stock. In times of heightened and persistent demand uncertainty, it does not take too long before inventory is no longer an asset, but more a noose around a company’s neck.

In times of heightened and persistent demand uncertainty, it does not take too long before inventory is no longer an asset, but more a noose around a company’s neck

[1] measured by the rate of change of demand variability and demand volatility; *H1, 2025 has been a period of heightened uncertainty driven by the many sizeable tariffs directed by the US against global trading partners, “reciprocal tariffs” being the latest shell to drop in a scarred global trade-war landscape ; the impact of this on demand uncertainty (variability), already evident in many industry segments (based on direct and secondary data) is yet unfolding.

The dual-mandate of inventory, structural implications

This results in the “dual mandate” faced by the COO and team, balancing two important but opposing needs –

– Carry enough inventory, including buffers, so you fulfill customer orders as needed, as they arrive

And

– Keep Inventory levels low so you do not have too much capital (money) tied up in stock, to run your operations

Compare two companies (illustrative example) –

For example, Company “A” that is carrying $500 Million in average inventory to fulfill $1 Billion of Revenue in a quarter,

versus

Company “B” that’s carrying $300 Million in inventory to fulfill the same level of Revenue – i.e., $1 Billion in a quarter

Company B has a significant structural advantage over company A.

So, inventory reduction is not an arcane, tactical task only to be initiated due to a near-term blip. Go ask your Supply Operations leader[1] to drive down inventory by x% (40%, as in the example above). And everything will be fine.

It is a critical initiative to drive down the capital requirements that gives your company a structural capital advantage. This requires careful attention to details while keeping an eagle-eye on the goal.

If you get this right, you can go much faster up the revenue and growth curve, having more freed up capital via healthy margins to allocate to smart growth (Revenue generating) initiatives.

Get it wrong, and you will not even know something is amiss for a long time. Then things can turn ugly quickly.

Get it (Inventory initiative) wrong, and you will not even know something is amiss for a long time, and then things can turn ugly quickly.

But inventory reduction, especially in channel centered selling models, is even more complex and difficult, as our experience and research shows. This is true whether you manufacture in-house or utilize outsourced manufacturing.

Status quo is often the biggest enemy.

David Cote (ex- CEO of Honeywell) articulates this well with a short story of his experiences as CFO at GE’s major appliance business, in his book – Winning Now, Winning Later (see “References” section at the end).

David’s story provides broad brush strokes on the key leadership mandate and insights gained. As a part of Zyom, we have worked closely with our customers’ cross-functional Operations team and their leadership in the trenches. We have been focused on achieving similar results in operations process optimization for our customers’ operations at physical product companies.

A key part of our customers’ successes has been our ability to collectively dive into the demanding details.

And, in almost all cases, we have come away with surprising findings as we have rolled out our end-to-end planning and execution framework and Operations Management Support (OMS) software system across product companies. Companies that were at different phases of their growth and development cycle.

We do not have inventory reduction numbers that we can share here. What is clear is that by slashing the end-to-end planning cycles by over 80%[2], we helped them achieve significant capital efficiencies – something they had not experienced before. How?

Very briefly – by achieving increased process velocity, across a focused set of end-to-end processes.

by slashing the end-to-end planning cycles by over 80%, we helped our customers achieve significant capital efficiencies – something … not experienced before. How? .. by achieving increased process velocity, across a focused set of end-to-end processes

The sustained[3]structural cost advantages that customers gained has freed up scarce capital which can now be allocated to other critical initiatives. This gives them an unprecedented operating advantage.

[1] working with Channel Sales depending on where inventory is high

[2] Based on analysis conducted and vetted by our customers

[3] Cost advantages achieved are structural (lower inventory levels to ship out the same revenue), hence recurring

Inventory levels rising ? Watch out!

Inventory (specifically, Channel inventory) is a double-edged sword. On the one hand, maintaining near-optimal channel inventory levels provides a competitive edge by ensuring fast and cost-effective order fulfillment. On the other hand, if inventory levels creep up too high, it can quickly become a noose around your neck – a heavy financial burden.

Left unchecked, rising inventory can impair your company’s financial performance in the near to middle term. This due to carrying much higher inventory levels for the amount of revenue shipped.

In case revenue growth shifts or slows down, you will be left holding the bag on ship-loads of inventory (much of which must be written down or written off).

Longer term, this will push your company into a corner, impairing your competitive standing.

As a Chief Operations Officer, you must ensure your inventory optimization initiative always bubble up to the very top. Make this a strategic initiative. Ensure ongoing support from the senior leadership. Mobilize all team members. Ensure it’s not just a tactical one-off.

See the ‘Actions’ block below. Drop us a line. We can share a picture and real-life stories around that. This can help your cross-functional team visualize how our customers and other senior operations leaders have successfully tackled this challenge, steering clear of those insidious inventory icebergs.

Actions for the COO:

How is inventory connected with process cycle time?

How will increasing process velocity help us lower the overall levels of inventory (finished goods, raw-materials and semi-finished stock, work-in-process)?

How should we go about increasing process velocity (which end-to-end processes)?

Have we received any “outsider in” perspectives on how you are making decisions in your value network (not just your supply network) and its impact on inventory? how is it leading sub-optimal inventory?

To learn more contact us here, or below. Stay tuned. As always your comments are a gift to all.

1) (Book) Winning Now, Winning Later: How Companies Can Succeed in the Short Term While Investing for the Long Term Author – David M. Cote

Disclaimer: Generative AI (GenAI) was used in a limited way for improving clarity of sentences only for this article. GenAI was not used for composing any of the writeups on this site (including this one), nor for any data gathering. GenAI was used to generate both the pictures in this article. At this point of time, there is no plan to use Generative AI to generate new content on this site. Readers will be informed in advance if this changes.

Parts are super critical. For Product companies the sum-total of all parts is what ensures that the product using the part is ready to make and ship.

Many parts shortages can be painful – economically, and what your logo stands for to the markets it serves, and needs to be attended to quickly but carefully.

This article starts with a short story (fiction) based on real life events, of a major planning dilemma – faced at the onset of the pandemic in the auto industry, and weaves its way across Billions of dollars lost in a short period of time by many companies. Not so for a few other industry peers.

Why? What happened?

This article underscores the critical role of operations planning and execution, and highlights key elements that can be learned, and applied quickly to improve the supply chains of parts (components/ sub-assemblies), ensuring uninterrupted supply, no matter what.

Parts, parcels and people – these three words pretty much summarize the biggest and sharpest pain-points that have come in sharp focus as global supply chain convulsions continue in the aftermath of the onset of the covid19 pandemic.

Sometime missing parts can make a hole in your plans to ship product. However, if parts shortages are chronic and unrelenting, it inexorably leads to big holes in a company’s revenue. Left unchecked, it can get quite grim.

This article is focused on Parts and cursorily touches on the “people” aspects.

Parts are super critical. For Product companies the sum-total of all parts is what make the product whole, and ready to make and ship. Parts shortages, especially those that have a big impact across many products are painful – economically, and what your logo stands for to the markets it serves. And it needs to be attended to quickly but carefully.

“A major Planning dilemma”: of wait & wants – A short story, an outsized impact

First let’s start with a story (fictional) based on real-life events. Its Q1, 2020, and the pandemic has hit the world – first landing in a few countries, it soon spreads like a forest fire throughout the world. In its wake, it leaves ports, factories and other nodes and links of the global supply chain frozen out.

Now, let’s hone in on one industry – the Automotive industry – that’s been recently feeling the tailwinds of growing consumer demand.

Jill, (fictitious name) head of Materials (parts, raw materials) Planning and Tier1 Supply, is feeling anxious. She brings this up again and again with her supervisor – the SVP of Operations at AutoMax1 – a traditional automaker (OEM) that’s been turning its fortune around over the last year or so. A simplified graphical representation of an extended supply chain with multiple tiers of supply is shown here for reference (Auto supply chains are extended, multi-tier manufacturing supply chains, excluding distribution-only nodes)

Jill – “..Bottom has fallen out of the demand .. what should we do with the open P.O.s to the Tier1 suppliers?”

After quick deliberations, spreadsheets and even looking at systems, a decision is made.

Managers (across functions) – “Let’s just cancel the orders”.

Jill – “All the open orders, or a few?”

Pause. More discussions. Deliberations.

Managers (with inputs from senior leaders) – “All”

..

All Q1 and a big chunk of Q2, 2020 turns out be worst case scenario for demand, as predicted. Auto industry demand crashes. Other peers of Jill, and the SVP Ops at other car companies largely take similar or same actions. ..

Its late in Q2, 2020, and an anxious Tier 2 chipmaker calls in and pitches a contrarian scenario –

Tier 2 chipmaker – “Demand’s picking up .. it may pick up too fast .. we don’t know yet. Do you want to reorder (your chips)?”

Again, long pause. Jill is not sure. SVP of Ops is torn. Even management is at sea.

Finally, they decide – “no Thanks .. we’ll wait”.

Not all agree, but they are not the assertive voice/s.

..

Its late in Q3, early on in Q4, 2020 and demand is indeed picking up.

Exciting news for AutoMax1 management? Not really.

Jill and SVP of Ops are super anxious. They may have shot themselves on both their feet with their decision a few months ago.

They have already been testing the waters, started communications with the Tier1s and some key Tier2 suppliers – the ones that make the microcontrollers, or get it manufactured by the Foundries. These are the chips that go into nearly everything in their cars.

Suppliers have NO inventory. Nothing meaningful for a very long time – months, probably quarters.

And the foundries are not heeding their (the Tier2’s) calls for help either.

AutoMax1 gets their COO (even the CEO’s ready) on the line with the Foundry chief.

COO – “You’ve gotta help us out .. we need to ramp up and need these chips now.. This can’t wait a week let alone the months that you are quoting us”.

Chip Foundry Chief – “Sorry, we are really super booked. We cannot even fulfill all open orders from (our larger) consumer electronics companies.”

“They came way before you .. placed hard orders, and reserved capacity”. In effect, giant chunks of capacity are now gone.

AutoMax1 COO – “what can you do?”

Foundry – “Nothing really in the near term .. nothing material for the next 2-3 quarters.. we’re nose to the grindstone getting these orders shipped .. we’ll call you as soon as we see capacity open up ..”

A Famine

And that pretty much sums up what happened to a giant chunk of the auto sector in the 2nd half of 2020, and Q1, 2021, leading up to the President of the US and heads of state getting involved in ‘battling the Auto chip shortage problem’. Nothing helped. Not for the near to fuzzy midterm[1].

The chip industry, a notoriously cyclical industry, with high booms and terrible busts in demand and pricing, with its gigantic, capacity-intensive fabrication plants (fabs) were booked solid with orders from the consumer electronics industry, that came way ahead of these auto orders.

In fact, these competing orders had a higher priority for the right economic reasons – higher margin consumer electronics orders, that use leading edge technology, versus the Auto industry that’s been on the lagging edge for a while. Lagging, despite the move to EVs accelerating – with Tesla et al. clearly gaining ground in the auto-market through their simpler, super popular EVs. Anyway, that’s for a later write-up, not this one.

What happened next is quite well known. A mini-nuclear winter of sorts for the auto industry..

Thanks to chip shortages painful shutdowns ensued, first by car category (with lower or lower margin demand), then multiple categories, then manufacturing plants, then entire groups of plants and virtually most (traditional) auto-maker plants across giant swathes of the US and Europe.

A Feast (almost) in other places

Meanwhile, over in Japan, Toyota is humming along – and by the end of Q1, 2020 even guided a rosier shipments (Revenue) picture for the whole year.

Tesla, a tiny dot in the auto-manufacturing firmament a few years ago, is growing shipments every quarter – still small compared with traditional car industry volumes – but ramping up seriously (roughly 80% volumes year over year). And they seem to be unfazed too. In fact, Q4, 2021 turns out be eye-popping one – Tesla shipping way more than anyone would have predicted.

And that’s what brings us to the $500 Billion dollar question[2].

What happened?

How could Toyota, a large automaker, be resilient throughout 2020 and early 2021 (some of the pixie dust appears to have worn off since)?

It’s after all a traditional automaker with plenty of gas-guzzlers in its portfolio (i.e., cannot participate in the EV spike in market demand).

What has Tesla learned about making cars, parts and sourcing for their factories which their 100+ year rivals with their huge volumes (i.e., purchasing power) have not?

Learnings

First off – No, this article is not about the auto industry, the EV leadership of Tesla etc.

This article is about finer operating points (operations planning & execution) that many, even with decades of supply chain and planning experience, appear to have missed.

A clear disclaimer – what’s written here is a hindsight-based learning, a post-mortem, not specific to any industry. Sincere attempts have been made to remove all hindsight bias.

No claims are being made by the author (or teams he works with) that they could have done a better job at ‘predicting’ the rapid downswing in the ‘early pandemic’ days, and the rapid upswing in demand soon after, for those sectors that faced what’s been described above (including the auto industry).

This article focuses on some key supply chain operating principles and practices that may have to be dusted off, looked at afresh if not challenged outright, and other evolving approaches to managing manufacturing-intensive supply chains.

Here are a few –

Identify key parts – This is not a straightforward exercise of looking at your highest dollar parts. What multi-variable analysis needs to be done to determine “key” parts? What additional ‘decision filters’ should be applied?

Use “lean signaling” not lean inventory approach especially for key parts – Ideally disintermediate your supply chain (i.e., reduce number of tiers) at least for the newer products, if you can. In either case – with long, extended supply chains (Traditional automakers like GM, Ford, VW et al.) or shorter chain ones (like Tesla), ask this: How can I rapidly collaborate (not just communicate) with my significant N tiers of supply (where N is 1, 2 .. whatever)? What are best (if not optimal) inventory levels for key parts made by the TierN supplier? Is there a better way than legacy tools (EDI, spread-sheets like MS-Excel, Google sheets, etc.)? Are internet-based supplier portals adequate?

Determine inventory levels for key parts – Toyota built strategic buffers for their key parts where and when needed. Toyota instructed its suppliers to carry months of inventory where previously they used to carry weeks’ worth only, the latter being in line with lean principles that is core to Toyota operations. How to determine what inventory levels are right? How & when to adjust? What analysis needs to be done rapidly? Which analysis can have longer cycle times?

Build real ‘relationships’ with suppliers (Tier2 and their sources, as needed) – Component (part) makers would love to work directly with the product makers (the ones whose logo goes on the product). This could be especially critical for mid-size and smaller companies that cannot command part makers’ attention via large, strategic buys. They know full well that one such wrong decision can put them into a deep working capital hole for a long time, or push them into extinction. Which component makers? What meaningful processes can you collaborate on? What are “must-haves” to make sure collaboration works (data, process, decisions, metrics)?

Plan for business continuity all the time – Business Continuity Planning (BCP) is not just for isolated worst-case events, such as the Fukushima disaster that froze auto supply chains, Taiwan earthquake that rattled consumer electronics – including the large behemoths. BCP is an ongoing process effectively used by those that are succeeding to secure the supplies needed, no matter what. How will you do this (process, people, parts, partners)? What parts to focus on? Which products? Which ones to defocus from?

Understand your key parts very well (passing acquaintance isn’t enough) – Get to know the technologies that go into your key parts, especially complex/ line-stopping ones very well (e.g., batteries for EV makers, microcontrollers for automakers, WiFi chipsets for wireless equipment makers, etc.). Build the technology skills needed so you can turn on a dime and change product design if a part’s supply shortage becomes persistent. Which technologies (chip design, etc.)? What skills? How to motivate learning?

Design for resilience and responsiveness – Back to the story above: Jill, the planning lead and her supervisor, the SVP of Ops were at a standstill and could not take decision to increase the supply even when the chipmaker dropped hints. There could be many reasons. Here are a few –

Role of planning in the org: does it have the right level of visibility and sway with the executive team? i.e., could they have pushed a more aggressive supply plan without being worried about untoward consequences (i.e., losing faith of the management, or worse)

Skills – Has Master Planning/ MRP/ Capacity Planning and related supply side operations planning skills been rethought through and retooled, especially for extended and evolving supply chains? Has demand planning been rethought through? Planning must be thought through for end-to-end Demand and Supply Planning. And then rethought through periodically in light of changes.

People-centered Processes and collaboration – Did AutoMax1 have a comprehensive process (including S&OP) which they could use to avoid bias? How good was their supplier collaboration to ensure clear supply signals – strong and weak signals (e.g., chipmaker signals noted above)?

Tools – What’s the burden of legacy? Were they going to war with bubble gum and duct-tape to put together their plans? Many legacy systems are a lot clunkier, difficult to use and error-prone, given cloud and internet-native tools can be designed and tailored for operations. And they suck up not only time but a lot of people too.

System – Were they educated about responsiveness which is not a demand side or supply side approach but an end-to-end approach? End-to-end from Demand through to Supply planning – not as ‘islands of Planning’. Execution signals have to be inbuilt into Planning.

Scaling mindset – A scaling mindset means looking at the future to be an opportunity to grow in a planned manner. How do planners avoid the “hunker-in-the-bunker” mindset that’s the default, especially in operations planning when faced with extreme uncertainty like what happened at the onset of the pandemic – circa Q1, 2020?

Question Assumptions

When faced with unprecedented uncertainty past assumptions have to be questioned.

Good planners know every plan has in-built assumptions.

Great planners know when to question those assumptions out aloud, so management gets it loud and clear. In the above case of Jill and AutoMax1, did they listen to the skeptical, dissenting voices among procurement and supply planners. The planners/ procurement team members may want to understand the signal better from the supplier/s (the chipmakers saying demand is ‘perking up’) before giving their procurement plans a massive haircut.

Great Operations leaders know Planning is a critical ongoing process that requires smarts and creativity, and focused attention of the top management (CEO, COO, Leaders of Operations and Sales, Products).

and,

The more inputs the better, especially from outside the 4-walls of the company, e.g., Sales channels, Suppliers, et al.

Most importantly, the age-old truism – not to be wedded to “a Plan”.

Plan, by its very nature is a point-of-time output of the process and needs to keep changing to support smart execution.

While nothing is better (for planners and senior strategists) than having a “run rate” product base to plan, those deep into planning and its subsequent execution, and have seen a few seasons (i.e., are experienced) know that ’stasis’ (standstill) is the absolute opposite of good planning – the wrong place to be. It’s after all a “rate”, i.e., change over time.

Companies that use this time of uncertainty to upgrade their team’s skills and equip themselves with better processes and systems based on learnings above will have all the pieces in place to go for a stronger rebound when demand turns around, and catch the downdraft in their demand much earlier, preventing grave preventable losses (E&O among others).

[1] Derivative of estimates the current size of the chip industry and the auto-industry losses

[1] Estimates vary from 2-3 quarters to 6-8 quarters out from late 2021

Acknowledgments:

The author would like to thank Colin Todd and Fred Harried for some of the learnings mentioned, and to all the (customer) colleagues at Cambium Networks for in-depth discussions and working sessions with Zyom on some of the topics mentioned in the article; All of the above contains copyrighted materials from Zyom Inc. Please acknowledge this when using any of the content.

The tide is turning. Channel partners and key customers are moving fast to your products..

Just as you were preparing to hear the beautiful humming sound of a well-oiled Operating machine shipping products out – you hear some ugly, jarring noises –

‘Hot-selling product has gone on allocation’

‘Big Channel partners are getting frustrated, as lead times start creeping up’

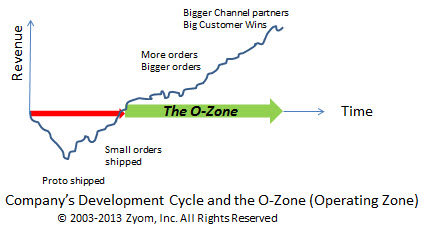

What happened? The Critical ‘O’-Zone

First, the good news – You have reached a major inflection point in your development cycle. You are no longer a small, obscure supplier waiting for the next large order. Orders are now waiting for you. Congratulations!

The not-so-good news – these orders will not wait long before they jump ship to a competitor.. Channel partners may divert attention to these competitors too.. So, what happened?

You just entered what we call the ‘O’ Zone (the “Operating” Zone). This is that part of your lifecycle (“zone”) when customers want to see you Operate like clockwork– shipping out 10x, 100x or more volume than before, yet meeting delivery dates globally, at attractive price points.

What happens in this vital phase of your Company’s development cycle is going to be determined in a big way by a critical collaboration – Near Real-time Collaboration between your Salesand Manufacturing/ Supply Chain Operations (Ops) team.

What’s causing these pains? No ‘growing pains’ is not a good label. Here is a critical one–

Divergent metrics & its impact on Sales & Operations

Your Sales team is focused on hyper-growth – signing up new Channel partners, winning new deals with end customers despite tough competition.

They are totally focused on order volume (Revenue) metrics, and compensated appropriately. So, they make sure they open up the gates and get more customers, more partners and more orders in. But hold on!

Do they have enough time to pivot to their Ops partners – give them a heads up about new customers, what product forecasts will be like?

Your Ops team, on the other hand, has an increasingly complex balancing act as demand takes off. They can grow their Supply Networks – to an extent (signing up new sources – new CM/ ODMs, new suppliers, etc.) to gain extra capacity, but then they hit the brick wall – of ‘Cost’ centered metrics.

The strains start to show in interactions between Sales & Ops.

The offshoot of all this is not pretty – As orders increase, Ops fulfillment can be in lock step only for a little while, after which demand and supply diverge. For Ops, it becomes a guessing game –

Q. What will Sales sell? How much buffer stock should we keep?

For Sales it becomes a hand-wringing exercise, as they field questions from customers –

Q. When will our orders ship? Why can’t you deliver it sooner?

With ‘Keep cost down’ as the guiding principle for Ops, it becomes a crazy dash to expedite when demand swings up with little notice, flying goods over instead of the more inexpensive modes (sea, rail or road) – depleting margins.

The human costs are bigger – anxieties mount as Sales & Ops try to play a game which looks somewhat like – catch the ball ‘blindfolded’.

Key to growth – A Vital, Systematic collaboration

In the O-Zone (operating zone) we need to play carefully – Pay special heed to the needs of this collaboration which is vital for growth –

Between Sales & Supply Chain Operations

To start off – Metrics need to be aligned.

How about rallying both Sales & Ops around ‘Profitable Growth’ metrics?

Let’s discuss it as a team at the leadership levels first. At a minimum – Sales, Supply Chain Operations, Operational Finance and you, should participate. The dividends of playing smart in the O-Zone are huge – Growth with Profitability – A distinct Operating Advantage. We, at Zyom, will be glad to help and explain further.

The most serious Risk that Companies with extended supply chains face is – the ShortageRisk. In the wake of the Japanese earthquake and tsunami[i], the floods in Thailand and a fire that took significant capacity of a critical automotive industry resin offline[ii] – ‘major supply shocks’ have taken center stage. But these are only a small subset of the Shortage risks that Companies and their Supply Chains face.

Often, the more mundane, ‘garden variety’ shortages that Companies face on a daily basis, can pack a vicious punch – making a serious dent in a company’s competitiveness, if not pushing it off the cliff!

Let’s understand why Shortages are the biggest risk now and examine potential warning signs that shortages maybe just around the corner.

The Destructive Impact of Shortages: For the want of a nail..

Shortages impact all companies downstream of the manufacturer facing shortages – to varying degrees. Sometimes, shortages can cut across industries.

For example, if Amazon buys up significant capacity of TFT glass (a specialized LCD used in different products) for its next new Kindle launch, that can cause shortages in unrelated industries – such as at video-game makers or electronic-toy makers. Even, the most agile Operations executives can get blindsided in such cases.

The impact of shortages can be severe. Dynamic young companies trying to ship products, stand to lose a lot. But even larger companies are not immune (Smartphone Biz Hurt by Own Success as Chip Supply Shrinks[iii]). Beyond the obvious Revenue impact, shortages can:

– turn away new customers (revenue hit),

– put-off existing customers (satisfaction erodes, loyalty and customer lifecycle value diminishes),

– cause unintended consequences (long lead-time for large companies downstream or an entire industry[iv])

– worse (perception of poor management controls, even if incorrect, adverse competitive impact[v])

Any one of these is bad enough. Their compounding effect can be devastating.

Avoid getting Blindsided – Warning Signs

At a time of such a tepid recovery, leadership across companies of all sizes should take note of this threat and ask – What are the warning signs that we are exposed? Here are a few critical ones we have found helpful:

1) Frequent over-forecasting by Channel partners and Field Sales – Manufacturing Operations team frequently asked to jump through hoops to increase shipment quantities at short notice, often to find later that forecasts were lowered.

2) Dependence on very few suppliers – OEMs totally dependent on few Contract Manufacturers (in the Hi-tech electronics industry) or Tier1 suppliers (in the Auto industry) who are also major suppliers for other competitors. BOMs with a high percentage of single-sourced items should also throw up red flags.

3) Visibility limited to key suppliers in the first tier of supply only– For an OEM this means having the ability to manage and monitor the performance of direct suppliers only, in the best case (CM/ODMs or Tier1 Suppliers [vii]), and no visibility beyond that[vi].

4) Frequent Allocations sometimes even on ‘run rate’ products – For products that start approaching stable sales patterns, alarms should go off if shortages occur, before these products go on hard ‘allocation’.

5) Quarterly Business Reviews (QBR) with suppliers showing ‘strain’ or going ‘too smoothly’– If QBRs with Supply Chain partners start showing strains due to unplanned costs,etc.– that’s an early warning. Dangers may also be lurking, if no disagreements arise.

6) Total time to respond to demand changes is unknown or too long – When it takes too long to answer – “How long will it take to ship a 10% upside?” or the range is too wide (“a few hours to a few days”) – that’s a red flag.

There are exceptions to the above. However, time and again, across different companies and industries we have found the above provide a good check-list to harden Supply Chain processes and systems against shortages.

Have you been part of a recent ‘shortage event? Did you see any other warning signs? Other Supply Chain risks that are bigger?

[i] Japan and the global supply chain: Broken links; The Economist; March 31st, 2011

")